Trustless systems aim to reduce reliance on intermediaries, such as banks and governments, by leveraging cryptographic algorithms and smart contracts to enforce agreements and transactions directly between parties.

This paradigm shift has profound implications for societal structures, governance, and individual autonomy.

Trustless systems are built on the premise that participants in a network can interact securely without needing to trust each other or a central authority. Instead, trust is placed in the integrity of the underlying technology — blockchain — to ensure that all transactions are transparent, immutable, and verifiable.

Blockchain technology fundamentally alters how trust is established and maintained in financial and other transactions by introducing the concept of trustless systems.

These systems operate without the need for mutual trust between parties involved in transactions, relying instead on cryptographic verification and consensus mechanisms to ensure transaction integrity and security.

o what is blockchain technology all about?

Blockchain technology allows participants in a network to own a piece of the network by hosting a node (a device on the blockchain). Blockchain is more than just a tool to enable digital currencies.

At its most fundamental level, it is a new, decentralized, and global computational infrastructure that could transform many existing processes in business, governance, and society. Business, governance, and society processes

Blockchain has the potential to transform how humans transact. It is a decentralized electronic ledger system that creates a cryptographically secure and immutable record of any transaction of value, whether it be money, goods, property, work, or votes.

This architecture can be harnessed to facilitate peer-to-peer payments, manage records, track physical objects, and transfer value via smart contracts.

Defining a Trusted or Trust-Based System

To understand a trustless system, it’s important to first understand a trusted or trust-based system, which is the world we live in today.

Here’s a simple illustration:

- When you deposit money in a bank, you trust the bank to hold it so you can access it when you need it.

- When you initiate a trade on Obiex, you trust that Obiex will execute the trade for you and not freeze trading of that asset.

- When you send money to a friend through PayPal, you trust that PayPal will put the money in your friend’s account, not someone else’s.

Trust-based systems are baked into our society, but they’re fallible.

Banks are intermediaries for storing wealth. This is a trust-based system because users trust the bank to give them the money when they withdraw it.

In a trustless system, individuals hold wealth themselves rather than having to access it through a third party.

What is a trustworthy system?

A trustless system is a system that does not rely on actors to behave in a certain way for the intended result to occur.

The system executes the action without relying on humans to do so. There is no intermediary party, like a bank or broker, moderating the event. You don’t have to worry if the person you’re interacting with can be trusted. The system creates trust for you.

No bank is required to hold your money, and no friar is needed to deliver a message. There is no middleman, intermediary, or facilitator. The code executes the task.

The trustless feature of blockchain has profound implications for various industries. It enables secure, transparent, and efficient transactions.

The blockchain’s distributed ledger technology makes it nearly impossible to alter transaction data without consensus from the network, reducing the risk of fraud, corruption, and manipulation. This characteristic is particularly beneficial in financial services, supply chain management, and any sector where the integrity of transaction data is critical.

Key Components of Trustless Systems in Blockchain

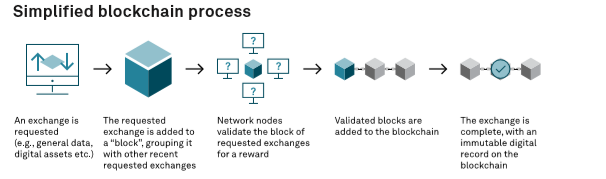

- Consensus Mechanisms: In a trustless blockchain network, the consensus mechanism — such as Proof of Work (PoW) or Proof of Stake (PoS) — ensures that all transactions are verified and agreed upon by the network participants. This means that individual members cannot break the rules or change them unless they utilize the appropriate channels. These mechanisms involve network participants, often referred to as miners or validators, who verify and agree upon the validity of transactions before they are added to the blockchain. This decentralized validation process ensures that transactions are secure and accurate without relying on a central authority, further enhancing the trustless nature of blockchain systems.

- Smart Contracts: Smart contracts are trustless systems. Blockchain technology uses smart contracts to facilitate trustless interactions between users. Smart contracts are immutable, meaning that once they have been deployed on the blockchain, a malicious developer cannot change the functionality of the code. So this system can be considered trustless because users trust that a malicious actor or developer can’t abuse their power and make a massive change in the project.

- DeFi (Decentralized Finance System): Decentralized finance (DeFi) is a blockchain-based financial infrastructure that has recently gained a lot of traction. The term generally refers to an open, permissionless, and highly interoperable protocol stack built on public smart contract platforms, such as the Ethereum blockchain. It replicates existing financial services more openly and transparently. In particular, DeFi does not rely on intermediaries and centralized institutions. Instead, it is based on open protocols and decentralized applications (DApps). Agreements are enforced by code, transactions are executed in a secure and verifiable way, and legitimate state changes persist on a public blockchain.

- Cryptographic Verification: At the heart of blockchain technology is cryptographic verification, which uses complex mathematical algorithms to secure transactions.

Each transaction is encrypted and linked to the previous one, creating a chain of blocks — hence the term “blockchain.” This encryption ensures that once a transaction is recorded on the blockchain, it cannot be altered or deleted without altering every subsequent block, which requires consensus from the network participants.

This makes fraudulent activities extremely difficult, if not impossible, thereby eliminating the need for trust in a central authority.

Trustless systems work and achieve consensus mainly through the code, asymmetric cryptography, and protocols of the blockchain network itself.

Blockchain's trustless environments enable peer-to-peer (P2P) transaction sending and receiving, smart contract agreements, and more.

How trustless systems achieve consensus and finality in the blockchain ecosystem:

How the Financial Sector is Redefining Trustworthiness

The concept of trust is undergoing a significant transformation, transitioning from trusted-based to trustless systems. This shift is facilitated by modern information technologies and has the potential to bring about substantial societal benefits and changes.

- Transition to Post-Modern Society and Trust in Technology: Modern information technologies have not only facilitated the transition to a post-modern society but have also challenged traditional views on trust. People have come to trust in technology via two primary constructs: human-like constructs, including benevolence, honesty, and competence, and system-like constructs, such as usefulness, reliability, and functionality.

- Influence of Societal Norms and Individual Characteristics: Trust in the finance area is deeply affected by societal norms and individual characteristics related to biological traits and personal history. Individual trust, rather than the average level of trust of the community, helps to retain the limited stock market participation observed in the data, especially among the wealthy.

- Value of Trust in Finance: Trust is important in the finance area for many reasons. It is positively correlated with economic development, and it has intrinsic and instrumental value that can benefit the trustor, trustee, or society in general.

- Challenges and Importance of Trust: The challenge in finance is having a conceptual framework and analytical way of evaluating and understanding trust. Without the proper framework, there’s no actionable way to improve trustworthiness.

- Legal Trusts and Financial Entities: In the context of finance, a legal trust is a complex entity with separate and distinct rights, similar to a person or corporation. It involves a trustor giving a trustee the right to hold title to and manage property or assets for the benefit of a beneficiary.

- Interpersonal Trust and Economic Development: Interpersonal trust differs across societies and plays a significant role in shaping economic development. There is a link between more inequality and less trust, which can be explained by the fact that people are often more willing to trust those who are similar to themselves.

- Trust in Banking: Trust is a crucial factor in banking, and aligning with cultural shifts and societal transformations is essential for a bank to be trusted. Banks that prioritize trust can design a self-reinforcing virtuous cycle because trustworthiness underpins growth and profitability.

Exploring Blockchain’s Impact on Finance

Decentralized systems, applications, and business models add a protective layer to the existing transaction infrastructure, enabling organizations to close the digital trust gap by helping them create a single version of irrefutable truth.

They rely on cryptography- and code-driven consensus of system-wide users rather than moderation by third-party intermediaries — without sacrificing data privacy.

The resulting shared, trusted record can be inspected by selected third parties but cannot be controlled by any single central superuser. A consortium of participants keeps the information up to date so that each participant maintains a copy of the updated, immutable database.

Trust-Related Use Cases

1. Digital Credentials: Individuals can own and manage their tamper-proof credentials for applications such as personal health, education, and voting records in an encrypted digital wallet on their devices. Proof of identification is stored in encrypted wallets for a more secure transaction.

According to Sandra Beattie, the state’s first deputy budget director, credibility with citizens was crucial: “We centered on the belief that the citizen owned their data and transactions and that our responsibility was to maintain the privacy and security of that data. Citizens had such a positive response to the app because they had trusted us to do that.

2. Digital Identities: People can leverage blockchain to create, manage, and store their identities in digital wallets, potentially leading to more secure transactions between sellers and buyers, landlords and prospective tenants, and even users of dating apps.

Businesses can verify or issue credentials, identities, and licenses.

For example:

the BMW Group partnered with the German government on blockchain-based driver’s licenses that help prevent identity fraud and reduce friction in transactions such as renting or purchasing a car and getting insurance.

3. External Data-sharing: Blockchain systems are useful for applications in which multiple external business partners, unknown or untrusted parties, or even competitors need to achieve consensus, and an intermediary isn’t wanted, needed, or feasible. By breaking down the data silos between such groups, blockchain allows data to flow among organizations without compromising privacy, security, or intellectual property.

For instance:

fashion brand LVMH launched the Aura Blockchain consortium to track the provenance of products to prove product authenticity; founding members include fellow luxury brands Prada, Cartier, and Mercedes-Benz.

Members develop their own unique experiences and maintain their data according to the strictest privacy standards.

4. Provenance and traceability: Businesses can provide tracking and tracing information about product provenance to ensure product and supply chain transparency.

Like LVMH and its founding partners, organizations in nearly every industry and sector are experimenting with blockchain to help them, their customers Nagano, a senior digital officer at JICA, says and other stakeholders track and trace information about the provenance of their products.

For instance:

the Japan International Cooperation Agency (JICA) used a blockchain-based system to monitor child labor on cocoa farms in Côte d’Ivoire. The project aims to make all aspects of the cocoa production process transparent, using blockchain to ensure traceability. Says Yushi Nagano, a senior digital officer at JICA, “The beauty of utilizing blockchain is in making an emotional connection from farmers in Côte d’Ivoire to consumers in Japan. Data technology is not cold; it can be warm and emotional, too.

5. Micropayments and transactions: New techniques can help streamline the micro-transaction intermediation process and reduce fees. When made in cryptocurrencies, online microtransactions — small payments ranging from a few dollars to even fractions of a penny, as in the case of in-game purchases — can carry transaction fees that are often greater than the transaction cost. New techniques can help make microtransactions more equitable by streamlining the intermediary process and reducing microtransaction fees.

Organizations are beginning to discover how trustless business models and operations could help them solve data-related credibility issues and win much-needed confidence across employee and customer groups, business ecosystems, and industries. There are also positive societal implications to consider.

Amid a crisis of faith in which seeing isn’t believing, and people can’t tell the truth from a lie, many of us have been waiting on a superhero: a person, company, or technology that might somehow serve as an unimpeachable arbitrator to help us settle quarrels and distinguish fact from fiction.

Decentralized, trustless architectures are beginning to teach us that we are the heroes we’ve been looking for and that none of us is as trustworthy as all of us.

The Power of Trustless Finance: How It Can Revolutionize Society

In our current trust-based world, transactions and systems go awry because we rely on humans to execute and maintain them for us. Instead of relying on human morals or middlemen, we can use trustless systems that execute and record events autonomously.

There is no fully trustless system because everything must be initially built by people.

Once the project is up and running on the blockchain, the smart contract cannot be altered. Traditional hierarchies are removed, and users with differing morals and values can still cooperate.

The transition to trustless finance enabled by blockchain has several potential societal benefits:

- Increased Financial Inclusion: Trustless systems can extend financial services to unbanked and underbanked populations, providing them with access to loans, savings accounts, and other financial products without the need for traditional banking infrastructure.

- Reduced Corruption and Fraud: By eliminating intermediaries and automating transaction verification through smart contracts, trustless systems can reduce opportunities for corruption and fraud, making financial transactions more secure and transparent.

- Enhanced Privacy and Control over Assets: In trustless systems, individuals have greater control over their financial assets, as transactions are peer-to-peer and do not require approval from a central authority. This can lead to increased privacy and autonomy over personal finances.

- Reduced economic inequality: By democratizing access to financial services, blockchain has the potential to reduce wealth concentration and increase social mobility.

- Increased transparency and accountability: Blockchain’s immutable ledger provides a clear record of transactions, reducing the risk of fraud and misconduct.

- Faster and cheaper transactions: By eliminating the need for intermediaries, blockchain-based transactions can be processed more quickly and at lower costs.

Challenges and Considerations

Blockchain offers promising solutions, but there are still challenges and considerations to address:

- Scalability and infrastructure: The underlying blockchain infrastructure needs to be scalable and versatile to handle large-scale financial applications.

- Regulation and governance: Policymakers and industry stakeholders need to establish clear guidelines for the use of blockchain in finance, balancing innovation with consumer protection.

- Adoption and interoperability: For blockchain to have a significant impact, widespread adoption and interoperability between different blockchain networks and legacy systems are necessary.

Conclusion

Blockchain technology revolutionizes the concept of trust in financial transactions by enabling trustless systems.

These systems leverage cryptographic verification, consensus mechanisms, and smart contracts to facilitate secure, transparent, and efficient transactions without the need for intermediaries. Thus, they reduce risks associated with fraud and corruption and promote greater financial inclusion.

While blockchain technology enables the creation of trustless systems, it’s important to note that trust is not eliminated but rather shifted — from people and institutions to cryptographic algorithms and code.

This shift requires trust in the integrity of the blockchain network itself, including its code and consensus mechanisms.

Vulnerabilities in smart contract code or malicious attacks exploiting these vulnerabilities highlight the importance of robust security measures, ongoing audits, and bug bounty programs to maintain the resilience of trustless systems against hacking and other threats.

Disclaimer: This article was written by the writer to provide guidance and understanding of web3/blockchain/cryptocurrency. It is not an exhaustive article and should not be taken as financial advice. Obiex will not be held liable for your investment decisions.